4

Second Quarter 2013

Industry Trends

(Aerospace)

Source: Public Filings; Industry Newswires and Capital IQ as of 06/28/13

6/30/2013

A320 Family A330/A340/A350 A380

5,109

4,014

938

157

Company

as of

Unfilled Orders by Aircraft Model

Totals

6/30/2013

737

747

767

777

787

4,757

3,445

53

56

339

864

The Aerospace industry’s focus is shifting to commercial markets, driven by defense budget cuts and an improving commercial growth

forecasts. In June the International Air Transport Association (IATA) increased its 2013 profit forecast for the global airline industry from

$10.6 billion to $12.7 billion, representing a 67% jump from 2012 profit of $7.6 billion. Faced by improved growth prospects and recent

mergers, airlines around the globe are looking to invest in more energy and cost efficient aircraft. In June, Boeing announced new

investments in its Commercial Airplanes business, including the planned establishment of engineering design centers in Washington, South

Carolina, and Southern California. Boeing also released commercial aviation projections of 34,000 new airplanes estimated at $4.5 trillion

over the next 20 years. Meanwhile, squadrons of military aircraft were grounded through most of Q2 and the F-35 faces added delays and

potential cuts.

Aircraft backlog for both Airbus and Boeing continued to expand and Airbus saw its backlog climb by 161 planes in Q2, driven by demand for

its A320 family. Boeing’s backlog grew by 312 aircraft, boosted by 320 new 737 orders. A growing demand for wide-body planes means

Boeing’s 787-10X and 777-8X/9X and Airbus’ A350 will likely benefit the most from the upcoming wave of orders for long-haul capacity.

Aircraft operators’ demand for greater cost and energy efficiency is increasingly being met by advances in propulsion and composite

materials. Innovations are creating stronger, lighter, and more fuel-efficient components offering overall efficiencies that encourage operators

to retire older aircraft and equipment earlier than scheduled. At the Paris Air Show (PAS) Pratt & Whitney’s new Geared Turbofan Advanced

(GTF) added 1,000 engines to its order backlog. The GTF burns 15% less fuel, 5% of which is due to the new gear and the other 10% due to

materials and component efficiency. CFM International, a joint venture by General Electric and Snecma, is utilizing carbon-fiber, ceramic-

matrix composites and other advanced materials to create fuel-burn improvements in conventional turbofans. At PAS CFM announced that

its Leap-1A engine has up to 3% lower specific fuel consumption than the GTF due to advances such as 3-D woven composite fan blades,

compressor variable bleed valves, and an uncooled ceramic matrix composite turbine shroud.

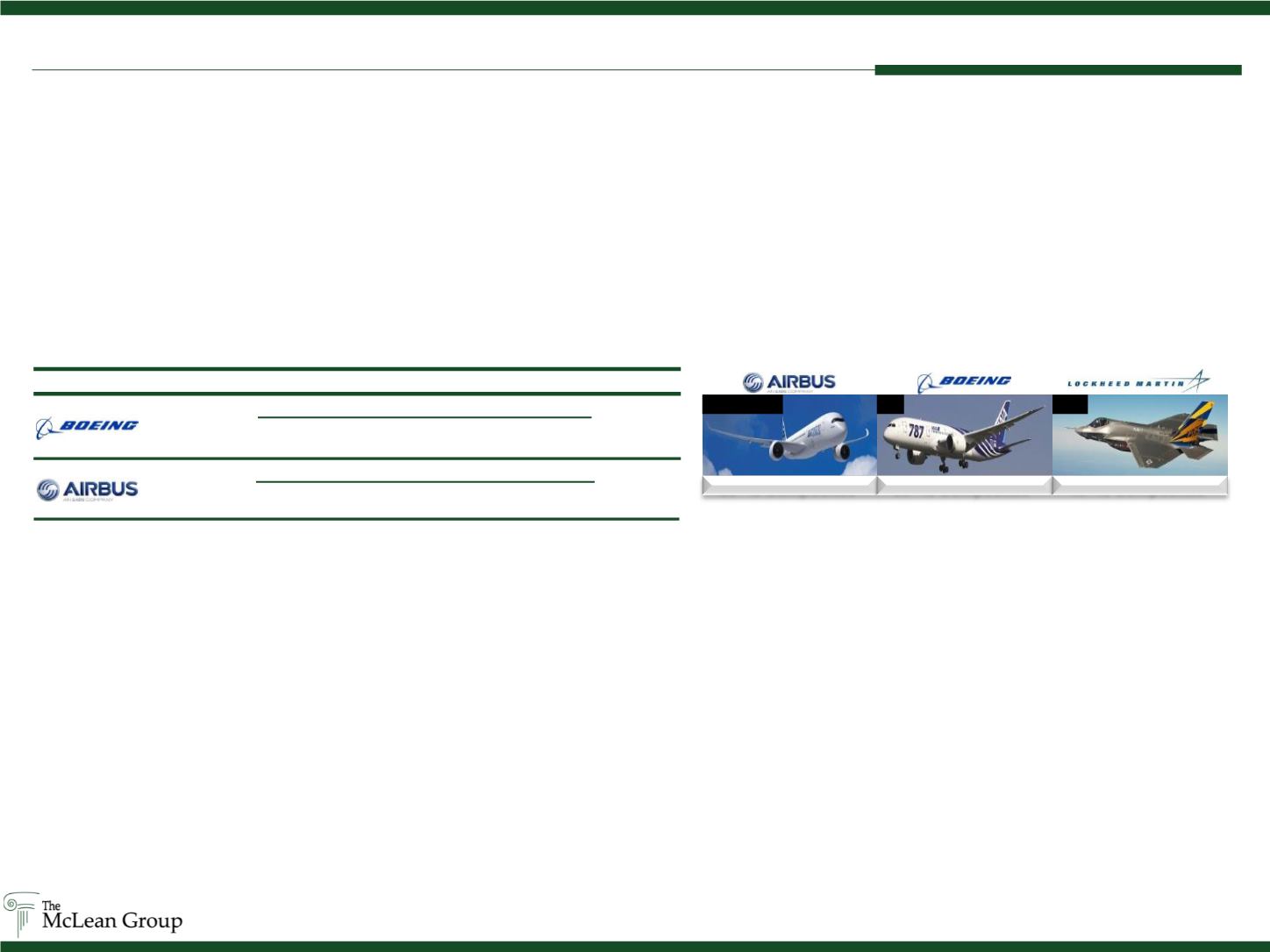

Likewise, OEMs are developing lighter and stronger airframes with composite materials. Composite have quickly overtaken metallic

applications on commercial aircraft, growing from just an average of 4-6% composite content by weight in the 1980s to 50+% on both the

Airbus 350 XWB and the Boeing 787. The Airbus 350’s fuselage panels, frames, window frames, clips, and door are made from carbon fiber

reinforced plastic (CFRP), with a hybrid door frame structure consisting of CFRP and titanium. Boeing’s 787’s airframe is nearly 50% carbon

fiber reinforced plastic and other composites, resulting in 20% less weight than the conventional aluminum design. On the defense side,

Lockheed Martin’s F-35 Joint Strike Fighter is manufactured with 40+% composite materials. Overall, the aerospace market for composite

materials is projected to continue its expansion from an estimated $2.3 billion in 2013 to $4.1 billion in 2016.

A350 XWB

787

F-35

50+% Composites

*

50+% Composites*

40+% Composites*

*Percent composite estimated as ratio of the aircrafts’ structural weight.